We normally think of intellectual property as a wall built to protect innovation. But there is an uncomfortable question hidden behind that wall. What happens when the person who creates an idea cannot afford to build the wall around it?

We normally think of intellectual property as a wall built to protect innovation. But there is an uncomfortable question hidden behind that wall. What happens when the person who creates an idea cannot afford to build the wall around it?

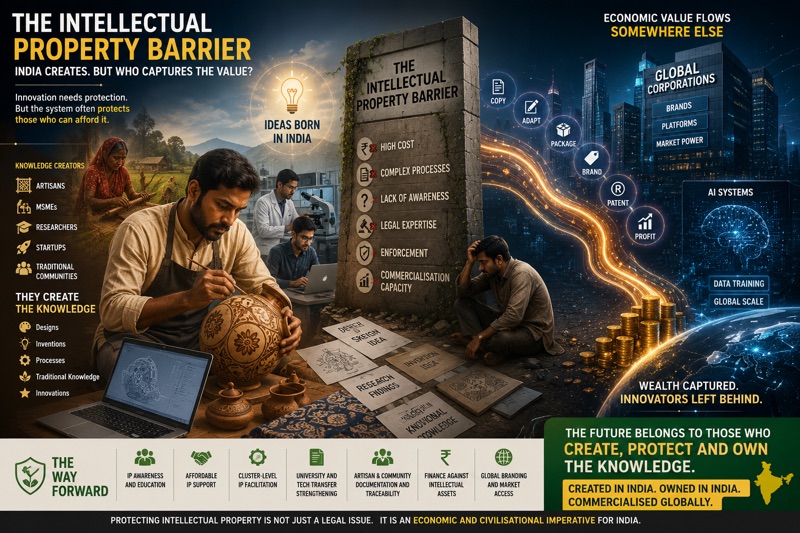

This is becoming one of the least discussed barriers in the modern economy. The future will increasingly reward knowledge, design, algorithms, brands, biological resources, traditional wisdom and specialised processes. But ownership of knowledge does not automatically belong economically to the person who created it. It often belongs to the person or organisation capable of documenting it, registering it, financing it, defending it and finally taking it to market.

That distinction could become extremely important for India.

India Has Always Had Knowledge. It Has Not Always Captured Its Value

For centuries, Indian communities developed sophisticated knowledge around textiles, dyes, metallurgy, agriculture, medicine, food processing, handicrafts and natural materials. Much of this knowledge was transmitted through families and communities rather than formal institutions.

The industrial economy changed the meaning of knowledge.

Knowledge gradually moved from being something people practised to something businesses could legally own, license and monetise. Patents, trademarks, copyrights, industrial designs and geographical indications became increasingly important instruments of economic competition.

The modern global economy has pushed this much further.

A product may cost very little to manufacture while its design, technology, software, brand and intellectual property account for a much larger part of its final market value. This means that countries can become excellent producers and still capture only a small part of the wealth generated by what they produce.

India therefore faces a deeper challenge than simply increasing patent registrations.

It must increase the economic ownership of innovation.

The Poor Innovator Problem

Imagine an artisan developing an unusual design. A small engineering company improves a machine component. A researcher develops a commercially useful technology. A farmer community possesses specialised knowledge about a plant. A small food enterprise develops a distinctive regional product.

All of them possess knowledge.

But possessing knowledge and converting knowledge into an economic asset are completely different things.

The innovator must understand what can be protected, search existing intellectual property, prepare documentation, choose the appropriate form of protection, file applications, pay professional expenses, monitor infringements, negotiate licences and potentially fight legal disputes.

For a large corporation, these activities are part of business strategy.

For a microenterprise, artisan or individual inventor, they can look like another profession entirely.

This creates a strange inequality.

The intellectual-property system may formally give everyone similar rights while economic capacity determines who can actually exercise those rights.

The Real Barrier Begins After Registration

India should also avoid measuring success simply through the number of patents, trademarks or geographical indications registered.

Registration is only the beginning.

An unused patent produces little economic transformation. A geographical indication without branding, quality control, producer organisation and market access can become little more than a certificate. A traditional craft protected on paper but sold through weak supply chains may continue generating low incomes for the people producing it.

The missing bridge is commercialisation.

India has universities, laboratories, startups, MSMEs, artisans and traditional knowledge systems generating enormous amounts of knowledge. But the institutional machinery connecting knowledge with capital, manufacturing, branding and markets remains uneven.

This creates what may be called the Intellectual Property Valley of Death.

Ideas are created on one side.

Markets exist on the other.

Many small innovators never cross the valley.

The Artisan Can Create the Design but the Market Can Capture It

This problem becomes particularly serious in India’s handmade economy.

An artisan may spend decades developing skills that cannot easily be reproduced through formal education. Yet a commercially successful design can sometimes be photographed, digitally reproduced, modified slightly and sold through larger distribution networks.

The original producer may remain invisible.

This is where the conventional discussion about intellectual property becomes inadequate. Traditional production is often collective. Designs evolve across generations. Knowledge may belong to communities rather than identifiable individuals.

Modern intellectual-property systems, however, developed largely around identifiable ownership.

The result is a mismatch between community knowledge and corporate-era protection.

A geographical indication can help, but GI registration alone cannot guarantee that the artisan receives greater income. Unless traceability, authentication, branding and market organisation accompany protection, economic value can continue accumulating elsewhere in the chain.

Protection without market power is weak protection.

AI Could Make the Problem Much Bigger

Artificial intelligence changes this debate completely.

The cost of copying, analysing and reproducing creative patterns is falling dramatically. Designs, motifs, product forms and visual languages can increasingly be digitised and processed at enormous scale.

A craft tradition that developed over several centuries could potentially become training material for digital systems within seconds.

The future intellectual-property conflict may therefore not simply be about one company copying another company’s product.

It could be about machines absorbing entire bodies of human creativity.

This creates difficult questions for countries such as India.

Who owns digitised traditional knowledge?

Who should benefit when culturally rooted designs contribute to commercially valuable AI systems?

How will an artisan in Kutch, Kashmir, Odisha, Rajasthan or the Northeast even know that elements of a traditional design have entered global digital production?

The technological ability to copy knowledge is becoming global while the ability to defend ownership remains highly unequal.

That asymmetry could become dangerous.

India Could Become a Knowledge Factory for Somebody Else

India wants to become an innovation economy. But there are two very different versions of that future.

In the first, Indian researchers, startups, artisans and enterprises create intellectual assets, commercialise them globally and retain a meaningful share of the resulting economic value.

In the second, India supplies engineers, researchers, designs, cultural knowledge, datasets and creative talent while intellectual ownership and high-value commercialisation increasingly accumulate elsewhere.

The second model can still produce employment.

But it may not produce sufficient economic power.

This is similar to an old development problem. Countries once exported raw cotton and imported expensive finished textiles. Tomorrow, the equivalent may be exporting raw knowledge and importing expensive intellectual property.

The commodity of the future may not be cotton, iron ore or petroleum.

It may be human intelligence itself.

We Need to Move from IP Registration to IP Infrastructure

India therefore needs something larger than awareness campaigns.

Intellectual-property support should become part of the economic infrastructure available to MSMEs, industrial clusters, universities, startups, artisan communities and rural enterprises.

Cluster-level IP facilitation could help enterprises identify protectable knowledge collectively. Universities need stronger technology-transfer capabilities. Research institutions need commercialisation professionals alongside scientists. Artisan clusters need design documentation, digital archives and traceability systems. MSMEs need affordable assistance for patents, trademarks, industrial designs, licensing and infringement monitoring.

Banks and investors must also learn to understand intellectual property as an economic asset.

Otherwise an unusual contradiction will continue.

A factory building can become collateral.

A machine can become collateral.

Land can become collateral.

But an innovative process, valuable brand or commercially promising patent may struggle to unlock finance.

That thinking belongs to the industrial economy of yesterday.

The Next Battle Is Not Simply Made in India

For decades, development policy concentrated on increasing production.

Then came the emphasis on exports.

The next stage will have to focus on ownership.

Who owns the technology?

Who owns the design?

Who owns the brand?

Who owns the customer relationship?

Who owns the data?

And who receives royalties long after the physical product has been sold?

These questions will increasingly determine where wealth accumulates.

India should therefore move beyond Made in India towards a much more ambitious objective: Created in India, Owned in India and Commercialised Globally.

That requires treating intellectual property not simply as a legal subject but as industrial policy.

The Most Dangerous Theft May Be Perfectly Legal

The greatest future danger is not necessarily somebody illegally stealing an idea.

It is something subtler.

A small innovator may fail to protect an invention. An artisan community may never document its knowledge. A researcher may publish commercially valuable work without a pathway to commercialisation. A traditional producer may remain unaware of international markets.

Then another organisation with better lawyers, capital, technology and distribution may transform that knowledge into a valuable commercial product.

Everything may happen within the rules.

Yet the economic reward may move far away from the original source of knowledge.

That is why the Intellectual Property Barrier is ultimately not just about patents.

It is about power.

The twenty-first century economy will increasingly be divided between those who generate knowledge, those who own knowledge and those who monetise knowledge.

India already has millions of people in the first category.

Its real challenge is helping far more of them enter the second and third.

Because in the economy that is emerging, producing the idea will not be enough.

The real wealth will belong to those who can protect it, own it and repeatedly earn from it.

#IntellectualProperty #Innovation #India #MSME #AI #TraditionalKnowledge #Handicrafts #Startups #Patents #MakeInIndia #EconomicDevelopment